Note

Access to this page requires authorization. You can try signing in or changing directories.

Access to this page requires authorization. You can try changing directories.

Azure Stream Analytics supports advanced analytics through the combination of SQL language, JavaScript user-defined functions (UDFs), and user-defined aggregates (UDAs). Advanced analytics include online machine learning training and scoring, and stateful process simulation. This article describes how to perform linear regression in an Azure Stream Analytics job that does continuous training and scoring in a high-frequency trading scenario.

Prerequisites

- An Azure subscription. If you don't have one, create a free account.

- An Azure Stream Analytics job.

- An Azure Event Hubs namespace and event hub.

- Familiarity with Stream Analytics Query Language.

- (Optional) A Power BI account if you want to visualize the output.

High-frequency trading workflow

The logical flow of high-frequency trading is:

- Getting real-time quotes from a security exchange.

- Building a predictive model around the quotes to anticipate the price movement.

- Placing buy or sell orders to make money from the successful prediction of the price movements.

This scenario requires:

- A real-time quote feed.

- A predictive model that can operate on the real-time quotes.

- A trading simulation that demonstrates the profit or loss of the trading algorithm.

Real-time quote feed

Important

The IEX trading WebSocket API (iextrading.com) referenced in this section has been retired. IEX Cloud now provides market data through IEX Cloud with different authentication and endpoints. Update the URL and authentication in your implementation accordingly.

Important

The SocketIoClientDotNet and WindowsAzure.ServiceBus NuGet packages used in this sample are deprecated. For new projects, use a current Socket.IO client library and the Azure.Messaging.EventHubs package with EventHubProducerClient instead of the legacy EventHubClient.

Investors Exchange (IEX) formerly offered free real-time bid and ask quotes by using socket.io. You can write a simple console program to receive real-time quotes and push them to Azure Event Hubs as a data source. The following code is a skeleton of the program. The code omits error handling for brevity. You also need to include the SocketIoClientDotNet and WindowsAzure.ServiceBus NuGet packages in your project.

using Quobject.SocketIoClientDotNet.Client;

using Microsoft.ServiceBus.Messaging;

var symbols = "msft,fb,amzn,goog";

var eventHubClient = EventHubClient.CreateFromConnectionString(connectionString, eventHubName);

var socket = IO.Socket("https://ws-api.iextrading.com/1.0/tops");

socket.On(Socket.EVENT_MESSAGE, (message) =>

{

eventHubClient.Send(new EventData(Encoding.UTF8.GetBytes((string)message)));

});

socket.On(Socket.EVENT_CONNECT, () =>

{

socket.Emit("subscribe", symbols);

});

Caution

This code sample is for illustration only. The IEX WebSocket API endpoint and the NuGet packages used here are no longer available. Don't use this code in production. See the IMPORTANT notes earlier in this section for current alternatives.

Here are some generated sample events:

{"symbol":"MSFT","marketPercent":0.03246,"bidSize":100,"bidPrice":74.8,"askSize":300,"askPrice":74.83,"volume":70572,"lastSalePrice":74.825,"lastSaleSize":100,"lastSaleTime":1506953355123,"lastUpdated":1506953357170,"sector":"softwareservices","securityType":"commonstock"}

{"symbol":"GOOG","marketPercent":0.04825,"bidSize":114,"bidPrice":870,"askSize":0,"askPrice":0,"volume":11240,"lastSalePrice":959.47,"lastSaleSize":60,"lastSaleTime":1506953317571,"lastUpdated":1506953357633,"sector":"softwareservices","securityType":"commonstock"}

{"symbol":"MSFT","marketPercent":0.03244,"bidSize":100,"bidPrice":74.8,"askSize":100,"askPrice":74.83,"volume":70572,"lastSalePrice":74.825,"lastSaleSize":100,"lastSaleTime":1506953355123,"lastUpdated":1506953359118,"sector":"softwareservices","securityType":"commonstock"}

{"symbol":"FB","marketPercent":0.01211,"bidSize":100,"bidPrice":169.9,"askSize":100,"askPrice":170.67,"volume":39042,"lastSalePrice":170.67,"lastSaleSize":100,"lastSaleTime":1506953351912,"lastUpdated":1506953359641,"sector":"softwareservices","securityType":"commonstock"}

{"symbol":"GOOG","marketPercent":0.04795,"bidSize":100,"bidPrice":959.19,"askSize":0,"askPrice":0,"volume":11240,"lastSalePrice":959.47,"lastSaleSize":60,"lastSaleTime":1506953317571,"lastUpdated":1506953360949,"sector":"softwareservices","securityType":"commonstock"}

{"symbol":"FB","marketPercent":0.0121,"bidSize":100,"bidPrice":169.9,"askSize":100,"askPrice":170.7,"volume":39042,"lastSalePrice":170.67,"lastSaleSize":100,"lastSaleTime":1506953351912,"lastUpdated":1506953362205,"sector":"softwareservices","securityType":"commonstock"}

{"symbol":"GOOG","marketPercent":0.04795,"bidSize":114,"bidPrice":870,"askSize":0,"askPrice":0,"volume":11240,"lastSalePrice":959.47,"lastSaleSize":60,"lastSaleTime":1506953317571,"lastUpdated":1506953362629,"sector":"softwareservices","securityType":"commonstock"}

Note

The time stamp of the event is lastUpdated, in epoch time.

Predictive model for high-frequency trading

For this demonstration, the sample uses a linear model described in Order Imbalance Based Strategy in High Frequency Algorithmic Trading.

Volume order imbalance (VOI) is a function of current bid/ask price and volume, and bid/ask price and volume from the last tick. The paper identifies the correlation between VOI and future price movement. It builds a linear model between the past five VOI values and the price change in the next 10 ticks. The model trains on the previous day's data with linear regression.

The trained model then makes price change predictions on quotes in the current trading day in real time. When the model predicts a large enough price change, it executes a trade. Depending on the threshold setting, a single stock might generate thousands of trades during a trading day.

The following sections show how to express the training and prediction operations in an Azure Stream Analytics job. The complete query is a single WITH statement composed of common table expressions (CTEs) that form a pipeline:

| CTE stage | Purpose |

|---|---|

typeconvertedquotes |

Convert raw input fields to proper SQL types |

timefilteredquotes |

Filter quotes to trading hours and remove invalid data |

shiftedquotes |

Use LAG to retrieve the previous tick's bid/ask values |

currentPriceAndVOI |

Calculate volume order imbalance (VOI) from current and previous tick |

shiftedPriceAndShiftedVOI |

Build sequences of 10 consecutive mid-prices and 2 consecutive VOI values |

modelInput |

Reshape data into feature vectors (VOI as x, price delta as y) |

modelagg / modelparambs / model |

Train a two-variable linear regression model using SUM and AVG aggregates |

shiftedVOI / VOIAndModel / VOIANDModelJoined |

Join current VOI values with the previous day's trained model |

prediction |

Calculate expected future price change (efpc) from the model |

tradeSignal |

Generate buy/sell signals when efpc exceeds the ±0.02 threshold |

Note

This query requires Azure Stream Analytics compatibility level 1.1 or later, which preserves field name casing for predictable behavior with UDAs.

Clean up and convert quote input fields

The first CTE in the Azure Stream Analytics query converts the raw quote data from Event Hubs into properly typed SQL columns. DATEADD converts epoch time (Unix milliseconds) to datetime. TRY_CAST coerces data types without failing the query. Cast input fields to the expected data types to avoid unexpected behavior in manipulation or comparison of the fields.

WITH

typeconvertedquotes AS (

/* convert all input fields to proper types */

SELECT

System.Timestamp AS lastUpdated,

symbol,

DATEADD(millisecond, CAST(lastSaleTime as bigint), '1970-01-01T00:00:00Z') AS lastSaleTime,

TRY_CAST(bidSize as bigint) AS bidSize,

TRY_CAST(bidPrice as float) AS bidPrice,

TRY_CAST(askSize as bigint) AS askSize,

TRY_CAST(askPrice as float) AS askPrice,

TRY_CAST(volume as bigint) AS volume,

TRY_CAST(lastSaleSize as bigint) AS lastSaleSize,

TRY_CAST(lastSalePrice as float) AS lastSalePrice

FROM quotes TIMESTAMP BY DATEADD(millisecond, CAST(lastUpdated as bigint), '1970-01-01T00:00:00Z')

),

timefilteredquotes AS (

/* filter between 7am and 1pm PST, 14:00 to 20:00 UTC */

/* clean up invalid data points */

SELECT * FROM typeconvertedquotes

WHERE DATEPART(hour, lastUpdated) >= 14 AND DATEPART(hour, lastUpdated) < 20 AND bidSize > 0 AND askSize > 0 AND bidPrice > 0 AND askPrice > 0

),

Retrieve previous tick values with LAG

The next CTE in the Azure Stream Analytics query uses the LAG function to get the bid/ask price and size from the previous tick for each stock symbol. One hour of LIMIT DURATION value is arbitrarily chosen. Given the quote frequency, you can find the previous tick by looking back one hour.

shiftedquotes AS (

/* get previous bid/ask price and size in order to calculate VOI */

SELECT

symbol,

(bidPrice + askPrice)/2 AS midPrice,

bidPrice,

bidSize,

askPrice,

askSize,

LAG(bidPrice) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS bidPricePrev,

LAG(bidSize) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS bidSizePrev,

LAG(askPrice) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS askPricePrev,

LAG(askSize) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS askSizePrev

FROM timefilteredquotes

),

Calculate volume order imbalance (VOI)

The next CTE computes the VOI value from the current and previous tick's bid/ask data. The query filters out null values for cases where no previous tick exists.

currentPriceAndVOI AS (

/* calculate VOI */

SELECT

symbol,

midPrice,

(CASE WHEN (bidPrice < bidPricePrev) THEN 0

ELSE (CASE WHEN (bidPrice = bidPricePrev) THEN (bidSize - bidSizePrev) ELSE bidSize END)

END) -

(CASE WHEN (askPrice < askPricePrev) THEN askSize

ELSE (CASE WHEN (askPrice = askPricePrev) THEN (askSize - askSizePrev) ELSE 0 END)

END) AS VOI

FROM shiftedquotes

WHERE

bidPrice IS NOT NULL AND

bidSize IS NOT NULL AND

askPrice IS NOT NULL AND

askSize IS NOT NULL AND

bidPricePrev IS NOT NULL AND

bidSizePrev IS NOT NULL AND

askPricePrev IS NOT NULL AND

askSizePrev IS NOT NULL

),

Build feature sequences for model training

The next CTE uses LAG again to create a sequence with 2 consecutive VOI values, followed by 10 consecutive mid-price values. These sequences form the training data for the linear regression model.

shiftedPriceAndShiftedVOI AS (

/* get 10 future prices and 2 previous VOIs */

SELECT

symbol,

midPrice AS midPrice10,

LAG(midPrice, 1) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice9,

LAG(midPrice, 2) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice8,

LAG(midPrice, 3) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice7,

LAG(midPrice, 4) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice6,

LAG(midPrice, 5) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice5,

LAG(midPrice, 6) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice4,

LAG(midPrice, 7) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice3,

LAG(midPrice, 8) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice2,

LAG(midPrice, 9) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice1,

LAG(midPrice, 10) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS midPrice,

LAG(VOI, 10) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS VOI1,

LAG(VOI, 11) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS VOI2

FROM currentPriceAndVOI

),

Reshape data into feature vectors

The next CTE reshapes the price and VOI sequences into feature vectors for a two-variable linear model, where VOI values are the independent variables (x1, x2) and the average future price change is the dependent variable (y). Events with incomplete data are filtered out.

modelInput AS (

/* create feature vector, x being VOI, y being delta price */

SELECT

symbol,

(midPrice1 + midPrice2 + midPrice3 + midPrice4 + midPrice5 + midPrice6 + midPrice7 + midPrice8 + midPrice9 + midPrice10)/10.0 - midPrice AS y,

VOI1 AS x1,

VOI2 AS x2

FROM shiftedPriceAndShiftedVOI

WHERE

midPrice1 IS NOT NULL AND

midPrice2 IS NOT NULL AND

midPrice3 IS NOT NULL AND

midPrice4 IS NOT NULL AND

midPrice5 IS NOT NULL AND

midPrice6 IS NOT NULL AND

midPrice7 IS NOT NULL AND

midPrice8 IS NOT NULL AND

midPrice9 IS NOT NULL AND

midPrice10 IS NOT NULL AND

midPrice IS NOT NULL AND

VOI1 IS NOT NULL AND

VOI2 IS NOT NULL

),

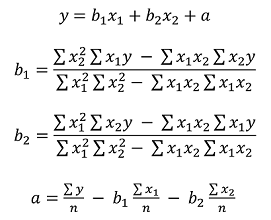

Train the linear regression model with SUM and AVG

Because Azure Stream Analytics doesn't have a built-in linear regression function, the query uses SUM and AVG aggregates to compute the coefficients (a, b1, b2) for the two-variable linear regression model. The model retrains daily using a 24-hour tumbling window.

modelagg AS (

/* get aggregates for linear regression calculation,

http://faculty.cas.usf.edu/mbrannick/regression/Reg2IV.html */

SELECT

symbol,

SUM(x1 * x1) AS x1x1,

SUM(x2 * x2) AS x2x2,

SUM(x1 * y) AS x1y,

SUM(x2 * y) AS x2y,

SUM(x1 * x2) AS x1x2,

AVG(y) AS avgy,

AVG(x1) AS avgx1,

AVG(x2) AS avgx2

FROM modelInput

GROUP BY symbol, TumblingWindow(hour, 24, -4)

),

modelparambs AS (

/* calculate b1 and b2 for the linear model */

SELECT

symbol,

(x2x2 * x1y - x1x2 * x2y)/(x1x1 * x2x2 - x1x2 * x1x2) AS b1,

(x1x1 * x2y - x1x2 * x1y)/(x1x1 * x2x2 - x1x2 * x1x2) AS b2,

avgy,

avgx1,

avgx2

FROM modelagg

),

model AS (

/* calculate a for the linear model */

SELECT

symbol,

avgy - b1 * avgx1 - b2 * avgx2 AS a,

b1,

b2

FROM modelparambs

),

Score current quotes with the previous day's model

To use the previous day's trained linear regression model for scoring the current event, the query joins the quotes with the model coefficients. Instead of using JOIN, the query uses UNION to combine model events and quote events into a single stream. Then it uses LAG to pair the events with the previous day's model, so you get exactly one match. Because of the weekend, the query looks back three days (72 hours). If a straightforward JOIN were used, you would get three models for every quote event.

shiftedVOI AS (

/* get two consecutive VOIs */

SELECT

symbol,

midPrice,

VOI AS VOI1,

LAG(VOI, 1) OVER (PARTITION BY symbol LIMIT DURATION(hour, 1)) AS VOI2

FROM currentPriceAndVOI

),

VOIAndModel AS (

/* combine VOIs and models */

SELECT

'voi' AS type,

symbol,

midPrice,

VOI1,

VOI2,

0.0 AS a,

0.0 AS b1,

0.0 AS b2

FROM shiftedVOI

UNION

SELECT

'model' AS type,

symbol,

0.0 AS midPrice,

0 AS VOI1,

0 AS VOI2,

a,

b1,

b2

FROM model

),

VOIANDModelJoined AS (

/* match VOIs with the latest model within 3 days (72 hours, to take the weekend into account) */

SELECT

symbol,

midPrice,

VOI1 as x1,

VOI2 as x2,

LAG(a, 1) OVER (PARTITION BY symbol LIMIT DURATION(hour, 72) WHEN type = 'model') AS a,

LAG(b1, 1) OVER (PARTITION BY symbol LIMIT DURATION(hour, 72) WHEN type = 'model') AS b1,

LAG(b2, 1) OVER (PARTITION BY symbol LIMIT DURATION(hour, 72) WHEN type = 'model') AS b2

FROM VOIAndModel

WHERE type = 'voi'

),

Generate trade signals from predictions

The final CTEs calculate the expected future price change (efpc) by applying the linear regression formula (a + b1 * x1 + b2 * x2) and then generate buy/sell signals based on a ±0.02 threshold. A trade value of 10 is buy. A trade value of -10 is sell.

prediction AS (

/* make prediction if there is a model */

SELECT

symbol,

midPrice,

a + b1 * x1 + b2 * x2 AS efpc

FROM VOIANDModelJoined

WHERE

a IS NOT NULL AND

b1 IS NOT NULL AND

b2 IS NOT NULL AND

x1 IS NOT NULL AND

x2 IS NOT NULL

),

tradeSignal AS (

/* generate buy/sell signals */

SELECT

DateAdd(hour, -7, System.Timestamp) AS time,

symbol,

midPrice,

efpc,

CASE WHEN (efpc > 0.02) THEN 10 ELSE (CASE WHEN (efpc < -0.02) THEN -10 ELSE 0 END) END AS trade,

DATETIMEFROMPARTS(DATEPART(year, System.Timestamp), DATEPART(month, System.Timestamp), DATEPART(day, System.Timestamp), 0, 0, 0, 0) as date

FROM prediction

),

Test the trading strategy with a simulation

After generating the trading signals, test how effective the trading strategy is without trading for real.

This test uses a UDA with a hopping window that hops every one minute. The grouping on date and the HAVING clause ensure the window only accounts for events that belong to the same day. For a hopping window across two days, the GROUP BY date separates the grouping into previous day and current day. The HAVING clause filters out the windows that end on the current day but group on the previous day.

simulation AS

(

/* perform trade simulation for the past 7 hours to cover an entire trading day, and generate output every minute */

SELECT

DateAdd(hour, -7, System.Timestamp) AS time,

symbol,

date,

uda.TradeSimulation(tradeSignal) AS s

FROM tradeSignal

GROUP BY HoppingWindow(minute, 420, 1), symbol, date

Having DateDiff(day, date, time) < 1 AND DATEPART(hour, time) < 13

)

The JavaScript UDA initializes all accumulators in the init function, computes the state transition with every event added to the window, and returns the simulation results at the end of the window. The simulation holds or shorts 10 shares of a stock per trade. The transaction cost is a flat $8. The following table shows the four trading actions the UDA performs:

| Condition | Signal | Action | Position after |

|---|---|---|---|

| No current holding | Buy (10) | Buy to open | Long |

| No current holding | Sell (-10) | Sell to open (short) | Short |

| Long position | Sell (-10) | Sell to close, then sell to open (short) | Short |

| Short position | Buy (10) | Buy to close, then buy to open | Long |

function main() {

var TRADE_COST = 8.0;

var SHARES = 10;

this.init = function () {

this.own = false;

this.pos = 0;

this.pnl = 0.0;

this.tradeCosts = 0.0;

this.buyPrice = 0.0;

this.sellPrice = 0.0;

this.buySize = 0;

this.sellSize = 0;

this.buyTotal = 0.0;

this.sellTotal = 0.0;

}

this.accumulate = function (tradeSignal, timestamp) {

if(!this.own && tradeSignal.trade == 10) {

// Buy to open

this.own = true;

this.pos = 1;

this.buyPrice = tradeSignal.midprice;

this.tradeCosts += TRADE_COST;

this.buySize += SHARES;

this.buyTotal += SHARES * tradeSignal.midprice;

} else if(!this.own && tradeSignal.trade == -10) {

// Sell to open

this.own = true;

this.pos = -1

this.sellPrice = tradeSignal.midprice;

this.tradeCosts += TRADE_COST;

this.sellSize += SHARES;

this.sellTotal += SHARES * tradeSignal.midprice;

} else if(this.own && this.pos == 1 && tradeSignal.trade == -10) {

// Sell to close

this.own = false;

this.pos = 0;

this.sellPrice = tradeSignal.midprice;

this.tradeCosts += TRADE_COST;

this.pnl += (this.sellPrice - this.buyPrice)*SHARES - 2*TRADE_COST;

this.sellSize += SHARES;

this.sellTotal += SHARES * tradeSignal.midprice;

// Sell to open

this.own = true;

this.pos = -1;

this.sellPrice = tradeSignal.midprice;

this.tradeCosts += TRADE_COST;

this.sellSize += SHARES;

this.sellTotal += SHARES * tradeSignal.midprice;

} else if(this.own && this.pos == -1 && tradeSignal.trade == 10) {

// Buy to close

this.own = false;

this.pos = 0;

this.buyPrice = tradeSignal.midprice;

this.tradeCosts += TRADE_COST;

this.pnl += (this.sellPrice - this.buyPrice)*SHARES - 2*TRADE_COST;

this.buySize += SHARES;

this.buyTotal += SHARES * tradeSignal.midprice;

// Buy to open

this.own = true;

this.pos = 1;

this.buyPrice = tradeSignal.midprice;

this.tradeCosts += TRADE_COST;

this.buySize += SHARES;

this.buyTotal += SHARES * tradeSignal.midprice;

}

}

this.computeResult = function () {

var result = {

"pnl": this.pnl,

"buySize": this.buySize,

"sellSize": this.sellSize,

"buyTotal": this.buyTotal,

"sellTotal": this.sellTotal,

"tradeCost": this.tradeCost

};

return result;

}

}

Note

The Power BI output connector for Azure Stream Analytics is scheduled for retirement. Consider using alternative output destinations such as Azure Data Explorer, Azure Synapse Analytics, or a data store that Power BI can connect to via DirectQuery or import. For more information, see Azure Stream Analytics output to Power BI.

Finally, output to the Power BI dashboard for visualization.

SELECT * INTO tradeSignalDashboard FROM tradeSignal /* output tradeSignal to PBI */

SELECT

symbol,

time,

date,

TRY_CAST(s.pnl as float) AS pnl,

TRY_CAST(s.buySize as bigint) AS buySize,

TRY_CAST(s.sellSize as bigint) AS sellSize,

TRY_CAST(s.buyTotal as float) AS buyTotal,

TRY_CAST(s.sellTotal as float) AS sellTotal

INTO pnlDashboard

FROM simulation /* output trade simulation to PBI */

Summary

This article shows how to implement a realistic high-frequency trading model with a moderately complex query in Azure Stream Analytics. The model uses two input variables instead of five because Azure Stream Analytics doesn't include a built-in linear regression function. However, you can also implement more sophisticated algorithms with higher dimensions as JavaScript UDAs.

You can test and debug most of the query, other than the JavaScript UDA, by using Azure Stream Analytics tools for Visual Studio Code for query development, testing, and debugging.